The Breast Network:

Why the Path to a Caris Two Hundred Dollar Stock Runs Through One Indication

I have been a Caris Life Sciences shareholder since near the IPO. I watched the stock go from the mid-twenties to $42.50 and back down to $15.50. This past week, someone replied to one of my posts on X: “Cai down… grail trending up… aged like milk.”

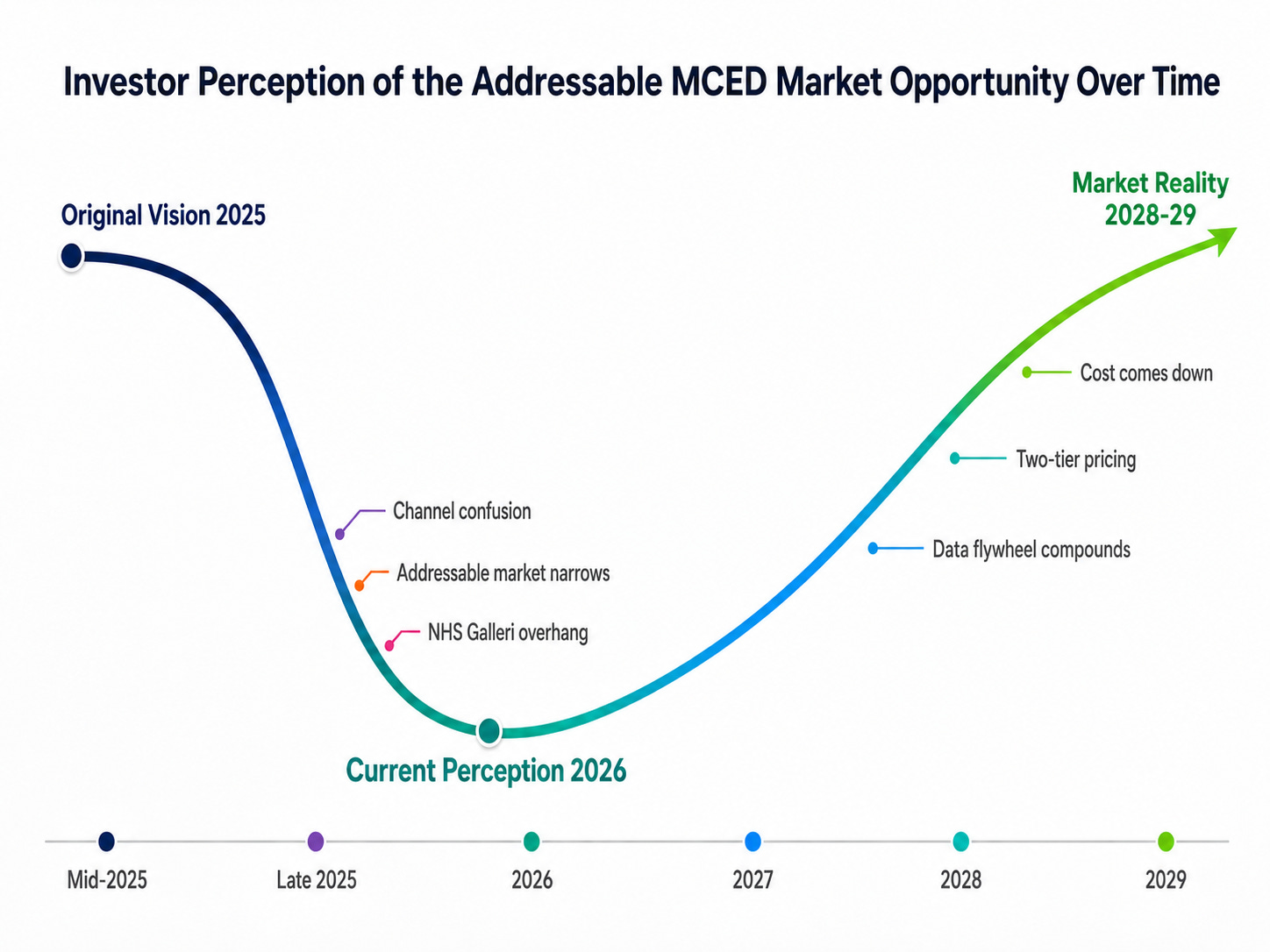

They were not wrong about the price action. GRAIL hit an all-time high of $116 in January, crashed into the low $40s after the NHS Galleri trial failed its primary endpoint in February, and has since recovered to around $68. Caris sits near its 52-week low. That asymmetry deserves an honest answer.

Here it is: the price action is real. The architecture the market is missing is also real.

Caris is not just building individual diagnostic products. In breast cancer, those products are beginning to connect into something more important: an integrated clinical pathway running from screening through profiling through recurrence stratification through longitudinal monitoring. No competitor appears to have the same end-to-end pathway in breast. The market is not pricing it. Until Caris names it clearly, I am not sure the market will.

The thesis, stated simply

Caris Detect, MI Profile, MI Clarity, and future MRD are usually discussed as separate products in separate markets with separate timelines. In breast cancer, they connect into a single patient relationship. That is the Caris Breast Oncology Network. Not a product bundle. A system.

The path to a much higher stock price may not require Caris to win every war simultaneously. It may require demonstrating one integrated pathway first, in the indication where the architecture is already most visible. The two hundred dollar discussion is not a price target. It is a valuation-ceiling argument: if the market starts pricing Caris as a clinical pathway and data platform rather than a collection of lab tests, the multiple changes. Breast cancer may be where that re-rating begins.

What the Caris Breast Oncology Network actually means

The concept is practical, not abstract.

For the patient: a woman does not enter for one test and disappear. She can enter through Detect as a dense-breast, elevated-risk, mammography-limited, or survivor-type screening patient. If a signal appears, she moves into imaging, diagnosis, and MI Profile for deep molecular understanding of the tumor. If she has early-stage breast cancer, MI Clarity helps separate early recurrence risk from late recurrence risk, two different biological problems that a single ten-year number does not resolve. Over time, MRD or longitudinal monitoring follows whether disease is returning or treatment is working. That is the A-to-Z pathway: screening, diagnosis support, profiling, recurrence risk, and monitoring. One system, one data layer, one compounding patient relationship.

For the oncologist or breast center: instead of stitching together separate vendors for screening, molecular profiling, recurrence scoring, MRD, and data infrastructure, Caris can become the integrated clinical layer around the patient. The oncology group gets data continuity across the breast cancer journey, a deeper molecular record, easier patient routing, research collaboration potential through the Precision Oncology Alliance, and a platform that generates clinical evidence over time. For the institution, the prize is not just fewer vendors. It is a cleaner clinical workflow and a richer longitudinal data asset.

The honest caveat is MRD. Caris does not fully own that layer today. Management has said MRD is now the next priority. Until the product is mature and reimbursed, Caris may need to partner, integrate, or route through a neutral MRD provider to complete the workflow sooner. The thesis does not require a specific partner. It requires the gap to be filled. Caris does not need more pieces. It needs to show the system.

The ethical quandary is real, but it is not a dead end

On the Q1 earnings call, an analyst asked whether Caris would consider a standalone breast test given that breast sensitivity in Achieve 1 was well above peers and the sample size was sufficiently large. The answer, delivered by David Spetzler and misattributed in the transcript, raised a legitimate concern: if the assay detects signals from multiple cancers, Caris should not suppress the non-breast findings.

An ethical dilemma is not a commercial dead end.

A breast-first product does not have to mean breast-only biology. It could mean breast-first positioning, breast-first reporting, and responsible safety-net disclosure of high-confidence non-breast findings above a meaningful clinical threshold. Patients could consent upfront to the reporting structure. Results could be routed through physicians or breast centers, allowing non-breast findings to be handled in a medically responsible way rather than through a pure wellness channel. The same underlying blood draw could support two commercial claims: a full MCED product for high-risk, survivor, and second-primary cohorts where comprehensive detection is medically justified today, and a breast-first adjunct screen for dense-breast women where breast signal interpretation is the primary clinical purpose. In my humble opinion the latter should sell at cost.

The ethical dilemma should shape the product. It should not kill the market.

Spetzler also made a second point in that answer that received less attention. He explained that lower sensitivity numbers in some other cancer types partly reflect the absence of effective screening infrastructure in those indications. Because many cancers are rarely found at early stage today, the training data skews late-stage, suppressing apparent sensitivity. As Detect gets deployed and starts finding early-stage cancers that currently go undetected, those numbers should improve over time. Caris would be generating the data that improves the test. No competitor with a narrower platform can replicate that flywheel.

A competitive week, compressed

The week was genuinely difficult for anyone trying to tell the simple version of the Caris story.

Guardant360 Liquid CDx received FDA approval as the largest FDA-approved liquid biopsy panel, combining genomic and epigenomic profiling from a single blood draw. Guardant advanced the liquid multiomics side. Natera’s oncology volumes grew fifty four percent year over year in Q1, Signatera CDx became the first FDA-approved companion diagnostic in blood-based MRD, and Natera is building what it describes as the world’s largest sequencing facility. The MRD volume story belongs to Natera in the near term. Tempus launched the ArteraAI Prostate Test inside its commercial ecosystem. Lucence is distributing through Mayo Clinic. AstraZeneca is building biomarkers in-house. Roche continues expanding its MRD infrastructure.

The field is crowding across every front Caris is pursuing. That is not a reason to abandon the thesis. It is a reason to understand why architecture matters more as competition intensifies. When every company has a liquid biopsy or an MRD product, the real question becomes who owns the deepest patient relationship and the most defensible clinical pathway. That is a different competition, and it is the one where Caris has the most complete answer in breast.

On MRD and the decision layer

Jason Carey, a precision medicine professional in medical affairs, made a pointed argument in a LinkedIn thread this week. He wrote that tissue-based molecular profiling and AI pathology are both snapshots taken at diagnosis, predictive models that cannot compare to persistent MRD negativity and ctDNA kinetics during longitudinal adjuvant monitoring. A senior oncologist echoed the direction publicly: a negative CT scan only tells you there are no visible tumors. One centimeter of tumor equals a billion cancer cells. CtDNA clearance, he argued, will eventually become a surrogate for overall survival.

Both are right about the direction. And both observations support Caris rather than weakening it.

MRD tells you whether disease is present. The deeper molecular platform helps answer what the tumor is doing, why it may be recurring, and what treatment options exist. Those are sequential clinical questions, not competing products. Detecting residual disease and knowing what to do about it are not the same problem. A binary detection platform has a structural ceiling when the question expands beyond presence or absence into treatment guidance and resistance prediction. Caris is building toward the decision layer above detection. That is where the network’s long-term value lives.

MI Clarity and the biology the market is ignoring

MI Clarity is not another recurrence score. The distinction that matters is this: early recurrence and late recurrence in breast cancer are not the same biological problem. A single ten-year recurrence number averages together two different disease behaviors that may require different clinical decisions at different points in the patient journey. Early distant recurrence tends to reflect aggressive tumor biology. Late distant recurrence, which can occur a decade or more after diagnosis in hormone receptor-positive disease, reflects a different set of molecular drivers. Averaging those two risks into one number is clinically misleading.

MI Clarity separates them. That is what makes it structurally different from the panel-based tests that preceded it.

The ECOG-ACRIN and SWOG collaboration with Caris on study EA1241 is not peripheral research activity. ECOG-ACRIN ran TAILORx. SWOG ran RxPONDER. Those are the landmark trials whose patient populations form the scientific foundation for genomic recurrence scoring in early-stage breast cancer. Those same cooperative groups are now directing one of the world’s largest breast cancer tissue banks toward a Caris collaboration to study what drives late recurrence years after diagnosis. That is the evidence infrastructure that supports guideline movement, payer coverage conversations, and clinical adoption. The network is the moat. Owning it requires naming it.

The ASCO picture

Caris is presenting 32 studies at ASCO this week across more than 60 institutions including Dana-Farber, Mayo Clinic, Memorial Sloan Kettering, and the National Cancer Institute. Roughly eight of those studies are breast-specific, covering recurrence patterns, CDK4/6 inhibitor outcomes in more than ten thousand ER-positive patients, ESR1 amplification and survival, BRCA pathogenic variants, resistance mechanisms, and treatment response predictors. George Sledge is hosting a fireside chat at the conference with former FDA Oncology Center of Excellence Director Richard Pazdur. Caris is debuting ChromoSeq and MI Clarity at their booth as newly launched products.

Natera is presenting 35 abstracts at the same conference, mostly concentrated around MRD detection across tumor types. The comparison is instructive. Caris’s presentations are distributed across the clinical decision questions that follow detection: what is driving this tumor, what treatment is likely to work, what resistance mechanisms are developing. That is the difference between a detection platform and a decision platform. The market is pricing Caris like the former. The ASCO abstract list reads like the latter.

Why the stock is here, and why the two-tier strategy matters

The stock is not at $15.50 because the profiling business is deteriorating. MI Cancer Seek volumes are holding. ChromoSeq carries a MolDX reimbursement rate of $3,228 for approximately 50,000 patients under the Medicare indications alone. Commercial payer submissions are already in motion, and the product runs through the same WGS/WTS infrastructure already in place. 50,000 patients at that rate is $161 million in addressable annual revenue. MI Clarity adds further at high gross margins. Cash flow is likely going up.

The stock is here because the MCED commercial strategy became harder for investors to read. The original framing pointed toward forty million dense-breast women as the near-term addressable population. Launching a test that Spetzler says already outperforms mammography through a DTC wellness channel made the strategy harder to interpret. The addressable market appeared to narrow to a smaller cohort of high-risk patients who could justify the full price today. Nobody pays a platform multiple today for a story the company itself seems to be pushing into 2029.

The answer is not to wait for costs to come down. The answer is two markets simultaneously.

The first market is the cohort that justifies a full-price MCED test today: second primaries and patients with a two to four percent annual cancer occurrence probability who need a broad test precisely because a cancer-specific screen is insufficient. These patients cannot afford to bet on one cancer type. The $3,500 price point is medically defensible for this population, and the reimbursement argument is far clearer than in broad average-risk screening.

The second market is the land grab. Caris Detect for dense-breast and elevated-risk women, priced at or near the cost of a Caris Assure blood draw, at zero or near-zero gross margin, as a volume entry into the breast oncology relationship. The goal is not immediate margin. The goal is installed base, clinical relationships, longitudinal data, and payer evidence.

The market currently gives Guardant and Natera far richer valuations than Caris, despite Caris having stronger profitability, because it is paying for commercial momentum and installed base. Caris should not be afraid to build one where it has the best architecture in the field. Breast cancer is where that build makes the most sense right now. Not because breast is the only market, but because it is the first market where the whole Caris architecture can be seen in one patient journey.

What needs to happen

I am frustrated because the company has the pieces and the market is not seeing the system. That is not only the market’s fault.

Caris has not publicly connected the dots in a way that makes the Caris Breast Oncology Network visible as a unified strategy. The individual products are being announced. The clinical evidence is accumulating. The institutional partnerships are forming. But the architecture has not been named.

There is a difference between announcing an MCED test, a recurrence score, a profiling platform, and a future MRD product and saying clearly: we are building the Caris Breast Oncology Network, the integrated clinical pathway that takes a patient from blood-based screening through molecular profiling through recurrence stratification through longitudinal monitoring without leaving the Caris data layer. The first framing is a product list. The second framing is a moat.

Caris does not need more pieces. It needs to show the system.

A note on what I know and what I do not

I am writing this as a shareholder working from public information. I do not know what management knows. I do not know the reimbursement constraints, product-labeling decisions, payer conversations, operational bottlenecks, or clinical sequencing decisions the way the people running Caris know them. There may be important reasons why my two-tier Detect idea is too simple, too early, or incomplete. I accept that. But that is also the point. Retail shareholders are trying to understand a complex company from the outside, and when the architecture is not clearly explained, the market defaults to seeing isolated products. If Caris wants retail investors to understand and explain the story intelligently, it needs to give them a clearer system to carry.

That is not a request for inside information or special access. It is a request for better public communication: retail-friendly product strategy sessions, clearer pathway explanations, more direct articulation of how Detect, MI Profile, MI Clarity, ChromoSeq, future MRD, and the Precision Oncology Alliance fit together into one clinical architecture.

The company does not need hype. It needs translation.

What the market may be missing

I may be wrong on details. The reimbursement path may be harder than I think. The two-tier pricing strategy may carry risks I am underestimating. The MRD gap still needs to be filled. The commercial timeline may be longer than the architecture suggests.

But the architecture is visible. And in breast cancer, it is more visible than anywhere else.

Caris does not need to become a breast cancer company. It needs to recognize that breast cancer may be the first indication where its full system becomes obvious to the market. Screening, profiling, recurrence stratification, and longitudinal monitoring are usually discussed as separate markets with separate vendors and separate timelines. In breast cancer, Caris has the pieces to connect them into one clinical network around the patient and the institution.

That is what the market is not pricing.

The network is the moat. The system is the story.

-----

I am long Caris Life Sciences (NASDAQ: CAI). This is not investment advice!